So, you’re looking for a new loan to buy new equipment for the workplace. But your credit report doesn’t look good. Now you’re worried that your loan application won’t be approved.

It’s not only about a loan application. The main problem is your business credit. You need to understand why your credit history looks so bad. Then figure out how to fix those problems for good.

Now, ready to repair your business credit? This detailed guide will help you throughout the credit repair journey!

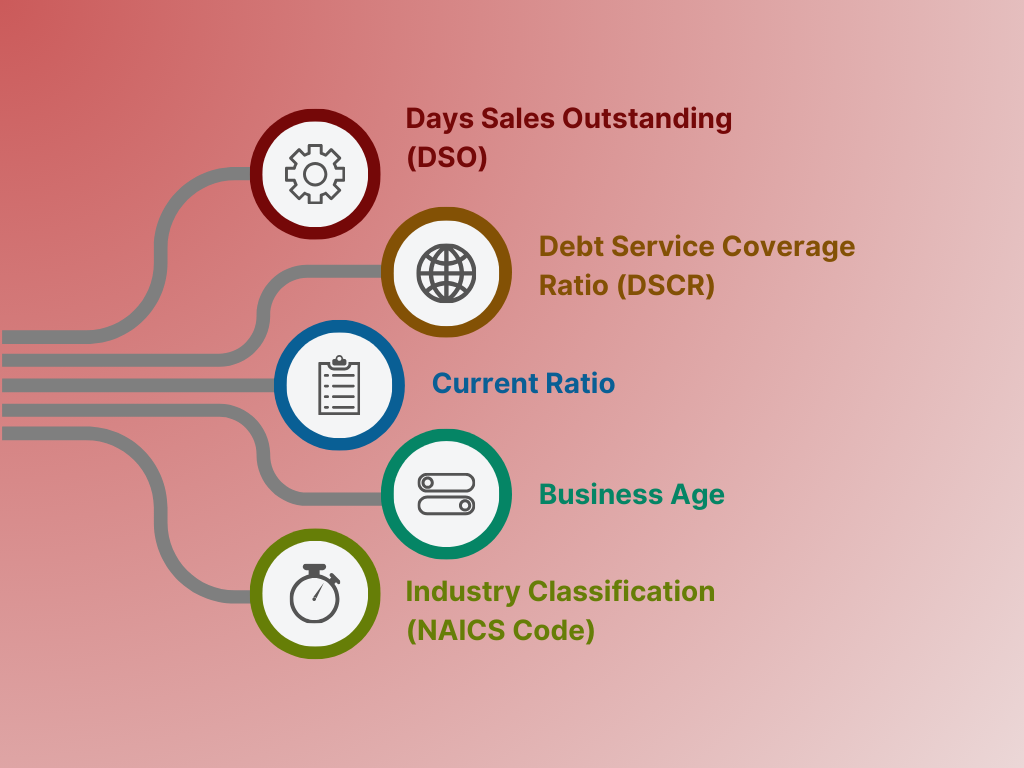

What Lenders See When They Analyze Your Credit

Are you ready to rebuild business credit? Then start thinking like a lender. Imagine you’re sitting on the other side of the desk. What would you see when you pull up your business profile on the screen?

Lenders don’t just check your credit score. They analyze multiple factors to paint a bigger picture. Here’s the information they usually see on their screens:

Days Sales Outstanding (DSO)

This shows how long it takes your customers to pay you. A high DSO means you’re waiting too long for your customers to pay you. These late payments may lead to cash flow problems. Lenders see a high DSO as a risk. So, it’s best to try to keep your DSO low.

Debt Service Coverage Ratio (DSCR)

The DSCR ratio tells lenders if your business earns enough to cover its debts. The formula to calculate this value is simple:

DSCR = Net Operating Income / Debt Payments

Is your DSCR below 1? Then it means your business doesn’t make enough profits to pay what you owe. Lenders prefer to see a score of 1.25 or higher.

Current Ratio

Your current ratio compares your current assets with your current liabilities. It shows whether or not you can handle daily business expenses.

Your assets include resources that generate income. This includes tangible and intangible assets like cash, receivables, buildings, patents, and more. While liabilities are what you owe in the short term.

A current ratio under 1 suggests your business may be struggling to meet obligations.

Business Age

How long you’ve been in business matters. Lenders trust businesses with some history.

If you’re new to the business world, you need a different approach. Businesses under two years old don’t get disqualified outright. Instead, you need better credit habits and supporting documents to build credibility.

Industry Classification (NAICS Code)

Your NAICS code tells lenders what type of industry you are in. But not all industries are treated the same.

Some industries like restaurants, trucking, and construction are riskier. Others, like professional services or IT, might get more favorable treatment. If your code is inaccurate or outdated, it can reduce your chances of getting funding. That’s because your business may look riskier than it actually is.

Factors That May Be Dragging Your Credit Down

It’s important to learn what bankers/lenders see on their screen when they check your business profile. This information can work as your starting point for rebuilding business credit.

So, start with the basics. Pull credit report from major bureaus. These bureaus include Dun & Bradstreet, Experian Business, and Equifax Business. You may notice some factors hurt your business credit:

- Using your business bank account for personal spending

- Late payments to vendors, lenders, or utility companies

- High balances on business credit cards or lines of credit

- Credit utilization ratio higher than 30% of your credit limit

- Having very few or no trade lines reporting

- Multiple loan or credit applications in a short period

- Frequent overdrafts or low balances in your business account

- Seasonal sales fluctuations making your cash flow look unpredictable

- Errors on your credit report

- Delinquent accounts, liens, or judgments

Create What Credit Bureaus Want to See

If you want to repair business credit, don’t just focus on removing the bad stuff. Instead, build the right business profile. Show the credit bureaus and lenders that your business is strong, stable, and trustworthy. Here’s how you can do it step-by-step:

Keep Your Revenue Steady

Credit bureaus want to see consistency.

A business that earns money regularly looks far more stable than one with wild ups and downs. So, don’t rely on 1-2 customers for revenue. Try to build a strong, loyal customer base. This will help you earn steady monthly revenue in the long run.

Work With the Right Vendors

Did you know that not many vendors report to credit bureaus? Some vendors only report if you pay late. That means they will only report negative things. So, you can’t get any benefits if you pay on time or early.

You don’t want to lose this opportunity if you’re doing everything right. So, choose the right vendors to build a good credit history.

It’s best to talk to vendors before signing a contract. Ask them:

- Which credit bureaus do you work with?

- What type of information do you report?

- Is there a minimum purchase or credit activity required before you start reporting?

- Will you notify me if I miss a payment before reporting it?

Choose vendors who report your good behavior, not just your mistakes. This will help you pick vendors who can contribute to your credit repair strategy.

Maintain a Healthy Bank Account

Your bank statements speak louder than you think. Lenders like to see a balance that can cover at least two to three months of operating expenses.

Also, avoid overdrafts. Your credit score will be hurt if there are overdrafts during the last three months. Deposit income regularly. And maintain this habit for 12 to 24 months. It’s best to set up automatic transfers to avoid missed payments or low balances.

Use Credit Smartly

Credit cards and business lines aren’t bad. But your credit score can go down if you misuse them.

Credit bureaus want to see that you use credit responsibly. You need a variety of credit types. Mix it up with vendor trade lines, lines of credit, term loans, and secured business credit cards to rebuild credit.

But keep your credit utilization under 30%. Always make payments on time. Further, avoid maxing out your cards. Smart, consistent credit use over time improves your business credit profile.

Keep Old Accounts Open

The longer your credit history, the better it is for your business credit repair journey. Thus, don’t rush to close older accounts. If those accounts are in good standing, that’s a bonus.

Lenders and bureaus aren’t only interested in what you’ve done in the last few months. They also want to see your long-term credit behavior. With old accounts, you can show good financial habits.

There may be some old accounts you no longer use. Keep them open. Also, try to keep them active with occasional small purchases.

Don’t Neglect Personal Credit

Are you a small business owner? Did you choose the right business structure – sole proprietorship, LLC, or other suitable option? Then it’s good for building business credit. But your personal credit score still matters.

If your business is new or doesn’t have much credit history, then your personal credit becomes more important. Many lenders check your personal credit.

Keep your personal credit score above 680. And make sure no recent bankruptcies or collections are showing up.

Monitor Credit and Focus on Business Financial Health

Building credit isn’t something you do once and forget. You need to be intentional. Keep an eye on your business credit reports. This will help you catch errors, fix issues early, and keep your credit profile in good shape.

But credit is just one part of your business’s financial puzzle. Focus on overall financial health for long-term success.

Manage your cash flow wisely. This will ensure you aren’t short on cash when bills are due. Also, build an emergency fund to handle slow months or surprise expenses. And invest in financial forecasting tools. This way, you can stay one step ahead.

When you combine strong credit with smart financial habits, you set your business up for better funding opportunities, stability, and growth.

Looking to take full control of your finances and grow your business? Subscribe to our newsletter for practical tips on building wealth that move you closer to financial freedom. Join our community of 140,000+ hustlers who are on their way to becoming future millionaires through our blogs, podcasts, and informative resources.